How do you make investment decisions? What influences our behaviour? In this article, we will explore why investors make bad choices, caused by common behavioural biases like the gambler’s fallacy, hot hand fallacy, FOMO, or herd mentality, and how to avoid them.

The Base of it All: Efficient Market Hypothesis or EMH

As Nobel laureate Eugene Fama proposed, a market is efficient if market prices reflect all relevant information about the underlying assets. In such a case, the market price is always identical to the fundamental value. If news releases impact the fundamentals, prices adjust immediately to take the new information into account. If Elon Musk influencing Doge Coin prices comes to mind here, you understood the concept.

But back to the theory. The efficient market hypothesis (EMH) can be classified into three forms:

1. Weak form: Past prices do not contain any information about future prices

The weak form implies that any efforts conducting technical analysis on predicting price movement would be in vain.

2. Semi-strong form: Prices accurately summarise all publicly known information

The semi-strong form attacks all research based on public information. It implies that it is impossible to take profits from studying any industry news or market analysis about cryptocurrency since the tokens’ prices precisely reflect all the publicly known information.

3. Strong form: Prices reflect all insider information and publicly known information

The strong form indicates that even the so-called ‘insider’ information is already incorporated in the prices.

If financial markets are as perfectly efficient as described by EMH, we should no longer hope to make profits from studying the financial markets. But fortunately, the reality is far more complex than this hypothesis.

Things are Always Changing: The Importance of Momentum and Value

The most obvious market anomaly refuting EMH is the momentum observed in market prices. Momentum refers to uptrends and downtrends in price movements: rising prices keep rising whereas falling prices keep falling.

This proposition rejects the weak-form EMH as it supports the correlations between future prices and current prices. Similarly, momentum trading, the corresponding strategy, means buying recent winners and recent short-selling losers.

Numerous studies have confirmed the persistence of momentum in diverse markets and asset classes.1 Recent research also concludes that the current returns of Bitcoin can predict its returns days and weeks ahead.2

How can we explain the existence of momentum in market prices? Economists have tried to explain momentum with underreaction and overreaction in the markets.3

There are typically three stages in the life cycle of a price trend. Here we assume that there are two groups of investors: news watchers who only react to the news and momentum traders whose trades are only based on past price changes.

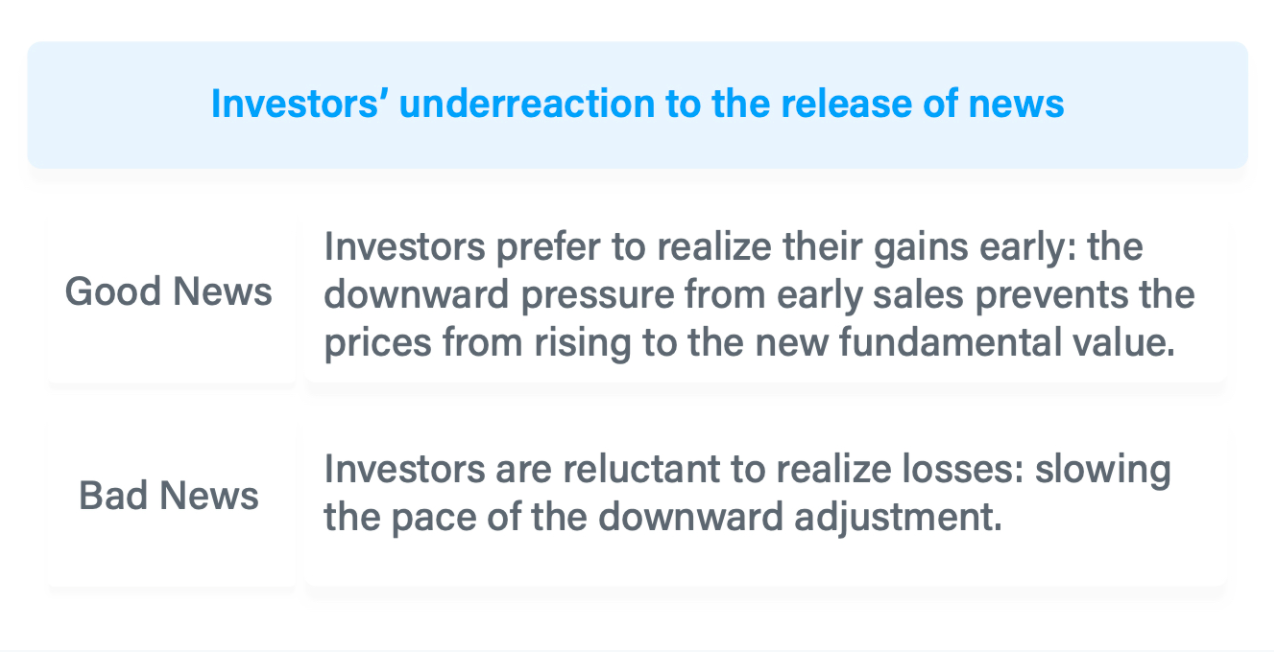

Stage 1: When a piece of good news gradually spreads in a group of news watchers, they start buying in on the good news. The asset now has a higher fundamental value, which measures the asset’s intrinsic ability to generate income in the future . The news watchers are value investors trying to profit from the difference between the new fundamental value and the current trading price. Initially, the price remains stable due to underreaction by stakeholders, but it slowly goes up to reflect the latest information. Such underreaction can be caused by human beings’ behavioural biases, which we will discuss more later.

Stage 2: Traders notice the slow uptrend and buy on it, pushing up the momentum. As more traders with herd mentality join the party, the price overshoots above the asset’s fundamental value, leading to a delayed overreaction.

Stage 3: When the market fully understands the news, the uptrend reverses, and the price finally converges to the fundamental value.

If the momentum is strong, a speculative bubble may form, and prices would plunge afterwards.

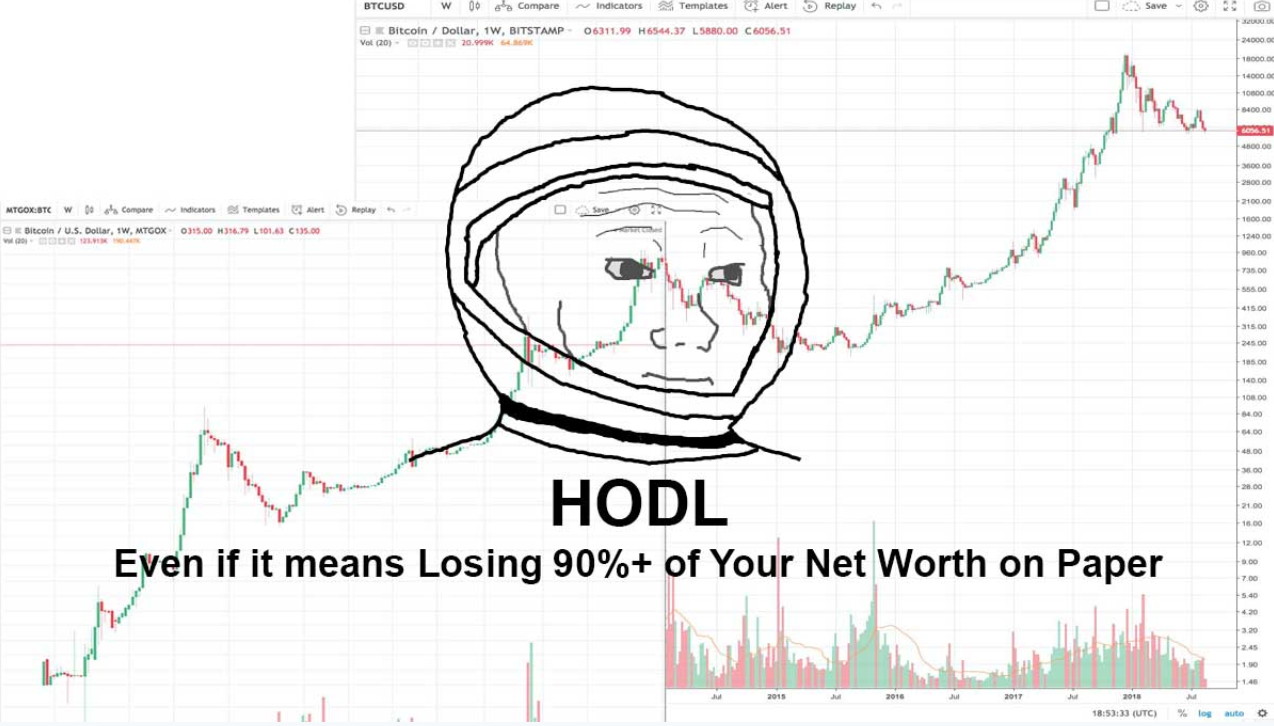

The boom and bust of bitcoin in 2017-2018 is such a case in point.

As the future potential of cryptocurrency and blockchain became better understood by the public, the bitcoin price was driven upward to reflect the fundamentals (stage 1);

and then more investors pushed up the momentum (stage 2).

Its price overshot its fundamental value, and the market also knew more about the current regulation, risk, and limitation regarding the asset. Fear, uncertainty, and doubt (known as FUD) spread in the market. Its price finally crashed (stage 3).

Behavioural Biases: The Disposition Effect and Prospect Theory

As the market is not perfectly efficient, some strategies are consistently profitable in the financial markets. These strategies, however, are easier said than done. The paradox here is that human beings’ irrationality partly creates room for such profits. We generally believe that we can make rational decisions, especially in trading and investment. Still, findings in behavioural finance have shown that we are probably overconfident, and we are susceptible to various biases.

An interesting phenomenon is that investors tend to sell winning investments too soon and hold losing investments too long.4 This is called the disposition effect, which explains why prices initially tend to underreact before the start of price momentum (see the previous chapter).

The famous prospect theory provides a framework illustrating the psychology behind the disposition effect.5

Let’s see how you are doing with this: ask yourself which option you would choose in the following two dilemmas:

1. Gain $900 for sure OR bet on a DeFi token: 90% chance of winning $1,000 and 10% chance of total loss?

2. Lose $900 for sure OR Bet on a DeFi token: 90% chance of losing $1,000 and 10% chance of zero loss?

In case 1, both options carry an expected gain of $900. As the second option involves a chance of total loss, a risk-loving person takes this option, whereas a risk-averse person picks the first option.

In case 2, both options have an expected loss of $900. As the second option involves a risk of larger loss, a risk-loving individual takes this option, whereas a risk-averse individual picks the first option.

The finding is that most people choose the first option in case 1 and switch to the second option in case 2. And their choices are not affected by how much money they own before making the choices.

The gist of the prospect theory is that individuals are generally risk-averse when facing potential gains, and they become risk loving when facing potential losses, and people are more sensitive to the pain from losing than the happiness from winning.

Some investors prefer to ‘HODL’ (buy and hold) crypto in the crypto world, as they try to stay away from short-term price fluctuations and believe in the crypto’s long-term growth in fundamentals. Investors may still ‘HODL’ in case of plunging prices since they think that irrational market sentiment drives the price far below its fundamental value. However, as illustrated by the prospect theory, they may be just reluctant to realise the loss, and thus they may lie to themselves that the market reaction is wrong. It is hard to separate market sentiment from fundamentals in reality, but we should beware of our loss aversion.

Mind the Trap: More Behavioural Biases

Besides the disposition effect, people have many other behavioural biases that can impact their investment decisions. Here we explore some of the interesting discussions.

1. Herding Behaviour and Fear of Missing Out

Here we elaborate more on the psychology causing delayed overreaction in the momentum story. Everyone jumps on board when the asset price is on a strong uptrend, and the hysteria pushes the price higher and higher. The herding behaviour is related to the ‘Fear of Missing Out’ (FOMO). Investors fear that they miss the profitable chances and are thus eager to buy on the trend. Such a mentality is not only found in retail and amateur investors. Institutional investors like mutual funds have also shown herding behaviour as they are afraid that their portfolio performances fall short of the market returns. FOMO is slang describing such investor sentiment in the crypto world.

2. Confirmatory Bias

People usually have a particular belief first. Then they search for information supporting their idea, which explains why sometimes they may see recent price movements as indicators of future price movements. Investors then buy more tokens that have recently made money and sell the tokens with a downtrend in price movement. Such behaviour can be self-fulfilling and help build up the price momentum. Another example of confirmatory bias is that investors with a bullish view of Tesla (TSLA) tend to read more articles sharing the same views.

3. Anchoring Effect

Anchoring is a perception bias that people may stick to historical information and adjust their views insufficiently to new information. Anchoring is an alternative explanation for the initial underreaction in the momentum story.

4. Gambler’s Fallacy and Hot Hand Fallacy

Gambler’s fallacy refers to the belief that the persistence of one signal in previous draws increases the chance of having another signal in the next draw. A simple example is that if you flip a fair coin and have ten tails in a row, you may think that you will probably be a heads in the next flip. Or, if the price of bitcoin has kept rising for ten consecutive days, you may expect that the price will retreat in the next day.

In contrast, the hot hand fallacy is the belief that a sequence will exhibit excessive persistence rather than reversals. Suppose a crypto commentator makes a streak of correct predictions on market movements for weeks. In that case, people may think this is an above-average commentator, and he/she will continue to make correct predictions.

The two above phenomena seem contradictory, but they are connected to the same statistical misconception.6 People tend to assume that what they observe in a small sample should be identical to the whole population from which the sample is drawn.

In the example of coin flipping, it is tempting to think that the number of heads will rise in the following flips such that the result is consistent with the expected result: 50% chance of tail and 50% chance of head. The reality is that people underestimate the likelihood of streaks in a small sample. In the commentator’s case, people infer from the small sample and conclude that the winning streak is strong proof of the commentator’s ability to outperform the market in long horizons.

While these studies, theories and explanations may seem more about psychological behaviour than practical tools for investment. However, they are key to smart investments, especially in the crypto world, where emotion and hype can play a big role in many peoples’ decisions. These theories can serve as reminders for us to stay vigilant to the market’s sentiment and our own biases in decision making.

So how Should You Invest?

Everyone has their own unique emotional responses to events in their lives, and responses to investment excitement and disappointment (or the fear of it) are no different. Hopefully, now you can, at the very least, step outside your emotional triggers to make the best, most rational investment decisions for you. One of the best ways to avoid being too swayed by emotional decisions is by ensuring that your portfolio management tactics is through understanding portfolio theory.

References

1. Asness, Clifford S., et al. “Value and Momentum Everywhere.” The Journal of Finance, vol. 68, no. 3, 2013, pp. 929–985.

2. Liu, Yukun and Aleh Tsyvinski. “Risks and Returns of Cryptocurrency.” NBER Working Paper, 2018, https://www.nber.org/papers/w20106.pdf.

3. Hong, Harrison, and Jeremy C. Stein. “A Unified Theory of Underreaction, Momentum Trading, and Overreaction in Asset Markets.” The Journal of Finance, vol. 54, no. 6, 1999, pp. 2143–2184.

4. Odean, Terrance. “Are Investors Reluctant to Realize Their Losses?” The Journal of Finance, vol. 53, no. 5, 1998, pp. 1775–1798.

5. Kahneman, Daniel, Thinking, Fast and Slow (New York: Farrar, Straus and Giroux, 2011), 280.

6. Rabin, Matthew, and Dimitri Vayanos. “The Gambler’s and Hot-Hand Fallacies: Theory and Applications.” The Review of Economic Studies, vol. 77, no. 2, 2010, pp. 730–778.